This Week’s CPI Report Could Be a Disaster for the Market

HadelProductions

This will be a make or break week for the market across all asset classes. Over the past few weeks, we’ve seen equities, rates, and the dollar drop significantly. Inflation data this week will suggest that the decline we see in The data on this point is about, which means that the sales so far are correct, or the data this week will suggest that the trends of the previous weeks are not worrying, leading to the reversal of the reduction that we have seen until now. .

However, based on market-based data and variables, the CPI data may confirm that the Fed’s rate-cutting cycle is about to begin in September. As a result, one can expect prices to fall, which leads to more harvests. More importantly, this will exacerbate the interest rate differential, leading USD/JPY to lower levels and continuing to liberalize commodity trading, which is bad for equity markets.

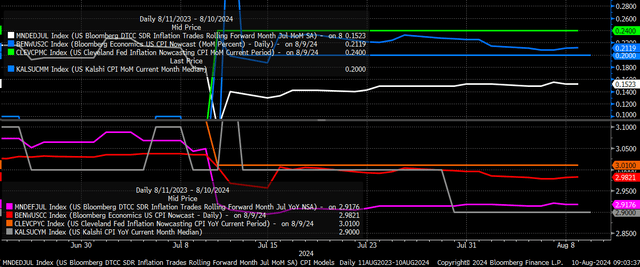

CPI Can Exceed

Analysts expect the CPI to rise by 0.2% m/m in July, compared to a decrease of -0.1% m/m in June. Meanwhile, the headline CPI is expected to remain unchanged at 3.0% y/y. Core CPI is expected to increase by 0.2% m/m, up from 0.1% in June and up by 3.2% y/y, down from 3.3% in June.

The market predicts, using CPI swaps, that the headline CPI will only rise by 0.15% m/m in July and by 2.92% y/y. If the exchange rate is correct, there will be a clear error in the headline CPI year-on-year, and that 0.15% increase is really close to calling, in terms of whether we get a 0.1% increase or 0.2% m/m.

Bloomberg

Some examples from Kalshi, the Cleveland Fed, and Bloomberg Economics suggest that the CPI, on a rolling basis, will not go above 0.2% m/m and not above 3% y/y. But more importantly, three out of four price models suggest that the headline CPI is coming in at 2.9% y/y, a clear error.

Bear Business Consequences

If the models are correct, this may suggest that the bearish trend that started in May is real. It may give the Fed the confidence it needs to start cutting rates in September. It is possible that this would result in short-term interest rates on the front of the US yield curve falling.

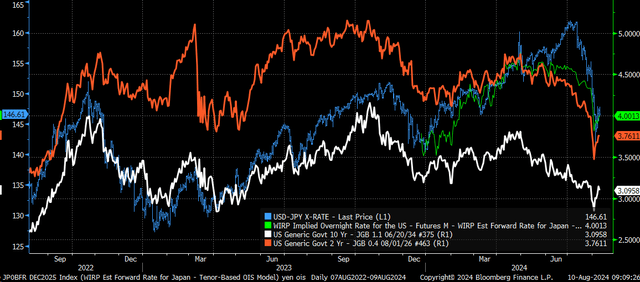

But more importantly, it will lead to a further conflict in the interest rate differentials between US Treasuries and Japanese Government Bonds. This further conflict may start to lower USD/JPY and reduce commodity trading. For example, this could cause the 10-year US yield to drop to the 10-year JGB, causing the spread or spread between government bonds to decrease, making the asset trade less desirable.

This past week was a good example because when interest rate spreads stopped their decline, USD/JPY stopped its decline. USD/JPY movements have more to do with US prices falling than BOJ hikes. Yes, the BOJ rate hike increases the cost of borrowing the yen, but falling US interest rates make the spread more volatile, making the trade less profitable.

Bloomberg

Harvest Harvest Harvest

Additionally, we’ve seen a big shift in the bond market, with the spread between the 10-year and 2-year falling, mainly because the 2-year rate is falling to the 10-year rate. Because the 2-year rate is was higher than the 10-year rate, the spread remained below -15 bps from July 2022, meaning the 10-year rate would not close the gap for two years. Hence, the recent move above the technical resistance at -15 bps is significant. It should support the yield rate going forward as the 2-year declines in line with expectations of the Fed’s interest rate cuts, and more importantly, it acts as a signal of slowing growth. of the economy.

Bloomberg

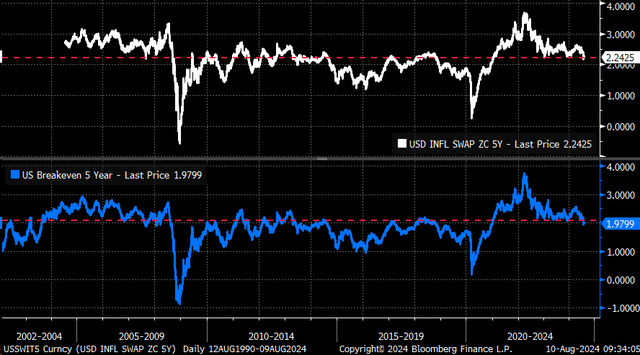

In addition, we have seen specific market-based financial instruments that measure inflation expectations, such as 5-year zero-coupon inflation swaps and 5-year zero-coupon inflation swaps, break some of the benchmarks. the importance of technical support. These levels of technical support held multiples for the past two years, even when it appeared that inflation would decline in the second half of 2023. This latest break of support appears to provide in the sense that the market thinks something has changed, not just in terms of inflation. but in terms of economic growth.

Bloomberg

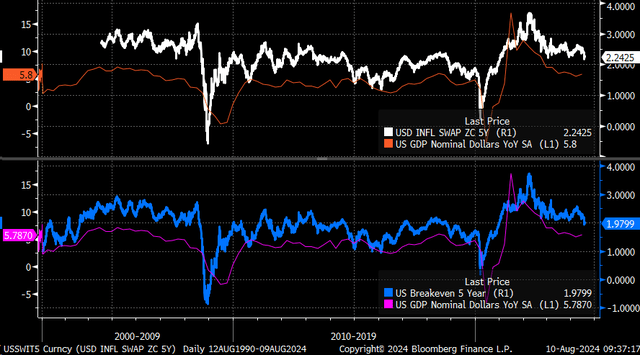

These measures of inflation expectations also track nominal GDP growth for a very long time over time, and a sudden drop in both measures can predict a further slowdown in inflation. economy in the coming months.

Bloomberg

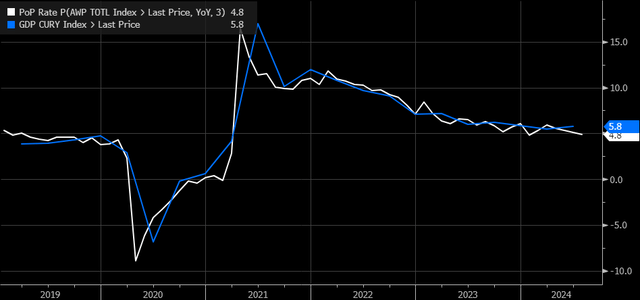

In addition, the July jobs report showed that the average weekly private sector earnings fell to 4.8% year over year, its lowest level since January 2024. It, too, tends to track GDP growth closely over time, suggesting a decline in nominal GDP. growth.

Bloomberg

Additional Risks

All of these changes signed before next week are likely to accelerate even more if the CPI data turns out to be weaker than forecast, as the swaps suggest is likely. This could lead to further appreciation of the yen against the dollar and a further increase in the yield curve. Because the rule of good news is bad news, bad news has become bad news.

A further relaxation of the yen trade and a sharp rise in yields will both be negative for the equity market, as it will continue to lower the long-term trade that has existed since March 2023.

If inflation data should come in hotter than expected, USD/JPY would rally, the yield curve would shift as short-term rates rise above long-term rates 10, and the stock market will be safe, at least for the long term. .

But again, CPI swaps, which are market-based, do not suggest a hotter-than-expected reading.

#Weeks #CPI #Report #Disaster #Market